Most attorneys begin their careers ready to argue cases and advise their clients. However, few are trained in the financial systems required to keep a law firm financially stable.

Bookkeeping for law firms goes far beyond recording income and expenses. It also involves managing client funds, maintaining trust accounts, and meeting strict ethical and regulatory requirements set by the bar. As a result, law firm bookkeeping requires a higher level of oversight and legal accountability.

Therefore, this guide explains how bookkeeping for attorneys works, its legal implications, and best practices to stay organized and compliant.

You can also work with specialized law firm accounting services like Karme to stay focused more on serving clients and less on managing financial records.

Why Bookkeeping for Law Firms is Complex

Bookkeeping for law firms is more complicated than bookkeeping for most other businesses. Law firms manage both their own business income and the money that belongs to clients. Because of this, law firms must follow state bar ethics rules in addition to standard accounting rules.

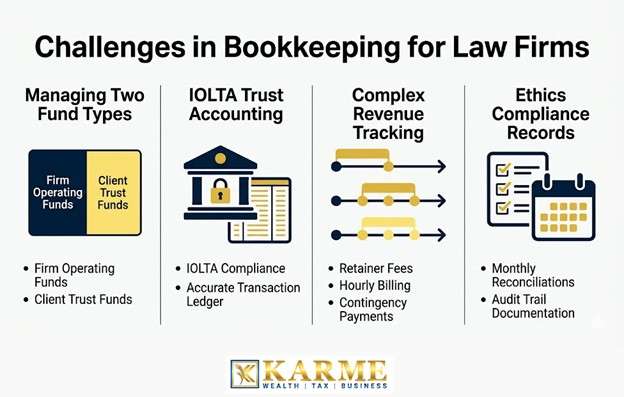

Here’s what makes bookkeeping uniquely complex for law firms

Managing Two Fund Types

Law firms must track the firm’s operating income and expenses while also managing client funds separately. Improper bookkeeping can lead to mixing of client money with the law firm’s own money, which can lead to serious penalties.

IOLTA Trust Accounting

Attorneys are required to keep client funds in special bank accounts called Interest on Lawyers’ Trust Accounts, commonly known as IOLTA accounts. Every deposit, withdrawal, and transfer to these accounts must be recorded carefully and linked to the correct client ledger.

Complex Revenue Tracking

Law firms earn revenue in different ways, which makes accounting more detailed. Some firms collect retainers before work begins, while others bill clients hourly during a case. Moreover, firms that work on contingency cases receive payment only after a court decision. Each payment method follows different accounting rules for when revenue can officially be recorded as income.

Ethics Compliance Records

State bar associations require law firms to maintain monthly trust account reconciliations, detailed client ledgers, and long-term records that go beyond IRS and GAAP standards. These standards are stricter than regular IRS requirements.

The Consequences of Poor Bookkeeping for Attorneys

Improper bookkeeping for lawyers can lead to trust accounting violations, which are one of the main reasons attorneys face professional discipline in the United States. The consequences can range from formal warnings and required training courses to suspension or permanent disbarment. In serious cases, attorneys may also have to repay money to former clients.

Common Causes of Trust Account Violations

According to the 2024 Florida Bar Discipline Trends report, trust accounting was one of the top three complaint categories handled by the Florida Bar in 2024. The same pattern was reported in North Carolina. According to the North Carolina State Bar Journal, 34% of attorneys cited for trust accounting violations mishandled abandoned client funds, and 24% failed to maintain the required reconciliation reports.

However, most trust accounting violations are not intentional but rather a result of poor bookkeeping. Common problems include:

- Monthly reconciliation reports that are missing signatures or dates

- Client ledger entries without proper documentation

- Mixing law firm operating money with client trust funds

- Failing to properly manage abandoned or unidentified client funds

Most of these problems can be prevented by using accurate and consistent bookkeeping practices.

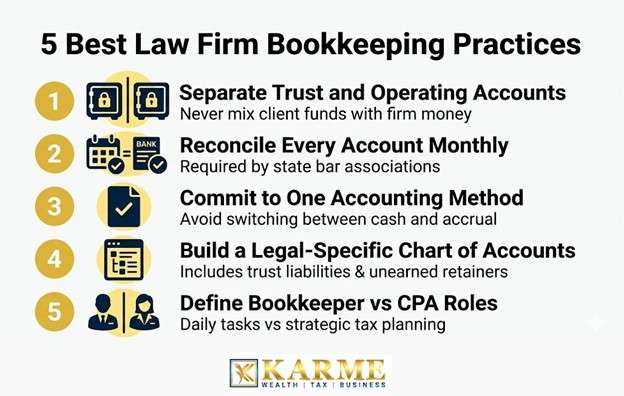

The Best Law Firm Bookkeeping Practices to Stay Compliant and Organized

Good bookkeeping helps law firms stay organized and avoid financial burden. The most effective approach is to keep clear financial records, follow consistent procedures, and assign financial responsibilities properly. Below are some important law firm bookkeeping practices to follow.

1. Separate Trust and Operating Accounts

Always keep your firm’s trust accounts and operating accounts separate. Money from a trust account should never be used to pay office expenses, including bank fees. This way, you can effectively protect client funds and ensure compliance with legal and ethical rules.

2. Reconcile Every Account Monthly

Monthly reconciliation is required by the bar association in many states. Therefore, compare the firm’s internal financial records with the bank statements every month to make sure all transactions are accurate

3. Commit to One Accounting Method

Most small law firms use cash-basis accounting, where transactions are recorded only when cash is received or paid. Switching methods mid-year creates inconsistencies, complicates reconciliations, and increases tax filing risks. Working with trusted tax preparation services can help you avoid tax errors and maintain accurate records.

4. Build a Legal-Specific Chart of Accounts

Standard small-business accounting systems often do not include categories that law firms need, such as trust liabilities, unearned retainers, and client cost advances. A legal-specific chart of accounts makes financial reporting more accurate and helps firms prepare for bar audits.

5. Define Bookkeeper and CPA Responsibilities

A bookkeeper handles daily financial tasks such as recording transactions, maintaining trust ledgers, and completing monthly reconciliations. A CPA is responsible for higher-level financial work, including tax planning and financial forecasting. Understanding the role of Bookkeepers vs. CPAs can help you choose the right financial support and maintain accurate financial management.

How Professional Legal Bookkeeping Services Can Help

A general bookkeeper may keep financial records accurate using standard accounting methods, but that is not always enough for a law firm. Law firms must follow additional rules for client trust accounts, state bar ethics, and specific methods for recognizing legal fees as revenue.

Professional Bookkeeping Services for Businesses can provide training and experience specific to a law firm’s accounting and regulations. They can help you:

- Maintain accurate client ledgers for all funds and transactions

- Reconcile trust accounts according to state bar rules

- Flag unusual transactions before they become compliance issues

- Generate clear financial reports on cash flow, unpaid invoices, etc.

When done right, these actions can directly translate into the following benefits.

- More attorney time available for billable work instead of financial tracking

- Lower risk of compliance violations due to consistent oversight of trust accounts

- Cleaner financial records that make tax filing and long-term financial planning easier

What to Look for When Hiring a Legal Bookkeeping Service

While professional expertise can be helpful, it’s also important to hire the right Professional Accounting Services for USA Firms Here’s what to look for before deciding:

- IOLTA and trust accounting expertise: The provider must have direct experience managing client trust accounts in compliance with state bar rules.

- Regular monthly reporting: The provider should deliver regular reports each month, including cash flow statements, accounts receivable aging, and other key financial summaries.

- Compliance Focused Processes: The bookkeeping service should design financial workflows to satisfy local, state, and federal mandates to minimize audit risks, keep payroll compliant, and ensure accurate tax filings.

Final Words:

Bookkeeping for law firms is essential for maintaining financial accuracy and meeting ethical and legal requirements. When attorneys manage their finances properly, they protect their law license, reduce compliance risks, and provide better service to their clients. Many law firms rely on professional bookkeeping support to handle these responsibilities correctly.

At Karme, we help law firms stay financially organized and compliant with industry regulations. Our services include trust account management, client fund tracking, compliance-focused bookkeeping, and detailed financial reporting. We also provide tax and accounting services, so your firm can manage all financial needs in one place. Get in touch with us today!

{kind=link}

{kind=link}

{kind=link}