Tax debt is money owed to the government after taxes go unpaid, underpaid, or miscalculated. It can happen to anyone: salaried employees, freelancers, small business owners, and retirees. What starts as a small shortfall can grow quickly due to compounding interest and IRS penalties, making the situation feel unmanageable.

The good news is that tax debt is resolvable. There are structured options to address your balance and get back on track regardless of how much you owe. This guide covers what tax debt is, why it happens, what the IRS can do if it goes unresolved, and which relief options may be available to you.

What Is Tax Debt?

Tax debt is the total outstanding balance a taxpayer owes to a government authority, typically the IRS at the federal level or a state revenue agency. It arises when the taxes you owe exceed what you have already paid through withholding, estimated payments, or credits.

Federal tax debt is generally more consequential due to the IRS’s broad enforcement authority. State agencies have their own collection tools but fewer resources than the IRS.

A tax debt balance is typically made up of three components:

- Unpaid taxes — The base tax amount not paid by the due date.

- Penalties — Charges added for failing to file, failing to pay, or underpaying estimated taxes.

- Interest — Accrued daily on the unpaid balance based on the federal short-term rate plus 3%.

Unpaid taxes grow quickly because interest compounds daily and penalties stack over time. A balance that seems manageable today can increase substantially within a few years, which is why early action matters.

Common Reasons People Owe the IRS

Tax debt rarely results from negligence alone. Most often it develops from changing life circumstances, misunderstood tax obligations, or situations that escalate before a taxpayer realizes it.

Underpaid or Unpaid Taxes

A common cause of IRS tax debt is not paying enough throughout the year. Employees rely on employers to withhold the correct amount, but life changes like a raise, a second job, or a spouse returning to work can shift that calculation. If the shortfall is not addressed before the filing deadline, a tax bill results.

Missing Tax Filing Deadlines

Failing to file by the deadline triggers a failure-to-file penalty on top of any unpaid balance. Many taxpayers assume that if they cannot pay, there is no point in filing. Filing on time, even without full payment, significantly reduces penalties.

Self-Employment Tax Obligations

Self-employed individuals must pay their own taxes quarterly. Without automatic withholding, it is easy to underestimate what is owed, especially when income fluctuates. Missing estimated payments results in underpayment penalties and a large balance at year-end.

Financial Hardship or Unexpected Life Events

A job loss, medical emergency, or divorce can make paying taxes impossible. When survival takes priority, tax payments fall behind. The IRS does not pause penalties and interest during hardship unless a formal arrangement is in place.

IRS Adjustments After an Audit

If the IRS determines that income was underreported or deductions were overstated, the additional tax liability becomes new debt. Responding promptly during an audit helps minimize the amount owed.

What Happens If You Don’t Resolve Tax Debt?

Ignoring tax debt does not make it disappear. The IRS has strong legal authority to collect what it is owed, and enforcement becomes more aggressive over time. Here is what to expect if a balance remains unresolved.

Penalties and Interest: From the moment a balance goes unpaid, IRS penalties and interest begin accruing. The failure-to-pay penalty is 0.5% of the unpaid balance per month, capping at 25%. Interest compounds daily on top of that.

Collection Notices: The IRS sends a series of letters notifying you of the balance. These notices include response deadlines and available options. Ignoring them accelerates the IRS collection process and limits your choices.

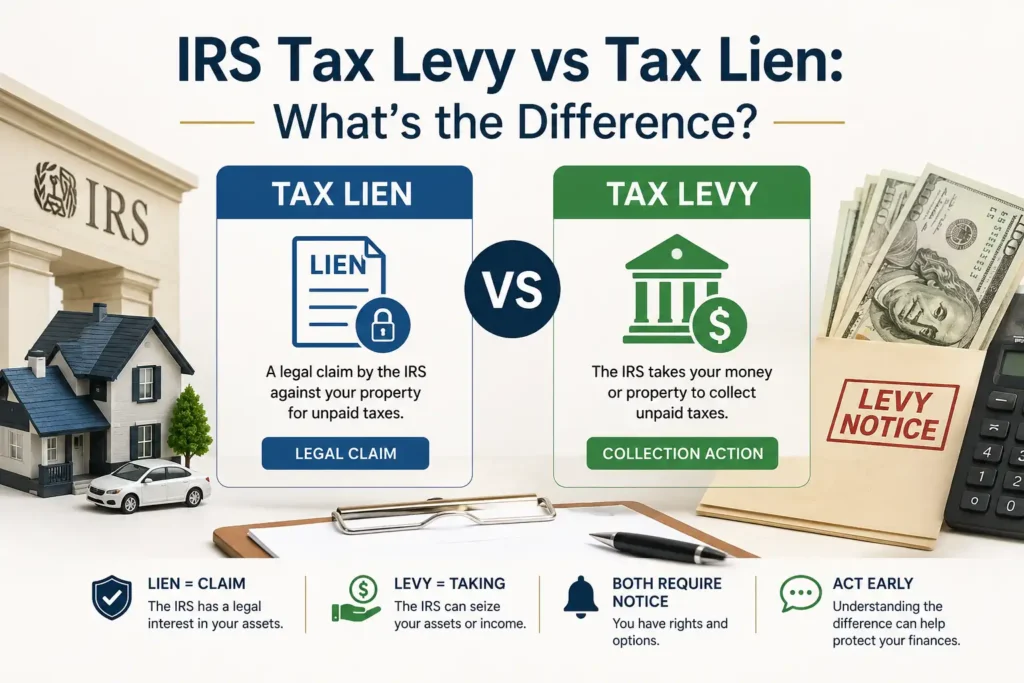

Tax Liens: If debt remains unpaid, the IRS may file a Notice of Federal Tax Lien. This is a public legal claim against your property, including real estate and financial accounts. A lien can affect your credit and complicate selling assets or obtaining financing.

Tax Levies and Wage Garnishment: A levy is the actual seizure of property. The IRS can withdraw funds directly from your bank account or issue a wage levy that directs your employer to withhold a portion of your paycheck. Unlike most creditors, the IRS does not need a court order to garnish wages.

Early action is always preferable. The further collection escalates, the fewer resolution options remain.

IRS Tax Debt Relief Options

There is no single solution that works for every taxpayer. The right approach depends on income, assets, filing history, and your specific financial situation. Below is an overview of the most common tax debt relief options.

IRS Payment Plans

IRS payment plans, formally called Installment Agreements, allow taxpayers to pay their balance in monthly installments. Short-term plans cover up to 180 days; long-term plans spread payments over several years. Having an active agreement generally prevents the IRS from pursuing levies or garnishment, as long as you remain current on payments and future filings.

Offer in Compromise

An Offer in Compromise (OIC) is a tax debt settlement program that lets eligible taxpayers resolve their debt for less than the full amount owed. The IRS evaluates your ability to pay, income, expenses, and asset equity before accepting an offer. Not everyone qualifies, and working with a tax professional significantly improves the chances of a successful submission.

Currently Not Collectible Status

If you cannot meet basic living expenses, the IRS may temporarily classify your account as Currently Not Collectible (CNC). Collection activity is paused, but the debt does not disappear. Penalties and interest continue to accrue, and the IRS periodically reviews your situation.

Penalty Abatement

The IRS may reduce or eliminate penalties under certain circumstances. First-Time Penalty Abatement is available to taxpayers with a clean compliance history. Reasonable Cause Abatement may apply when failure to file or pay resulted from circumstances beyond your control, such as a serious illness or natural disaster.

Eligibility for any of these programs depends on your individual financial situation. A qualified tax professional can help you determine which option is the best fit.

Tips for Preventing Future Tax Debt

A few consistent habits can help you stay ahead of your tax obligations and avoid future debt:

- File on time — Always file by the deadline or request an extension, even if you cannot pay in full.

- Pay estimated taxes — If self-employed, submit quarterly estimated payments to avoid underpayment penalties.

- Update your withholding — Review your W-4 after major life changes such as marriage, a new job, or a new dependent.

- Keep organized records — Clear documentation of income, deductions, and payments makes filing easier and protects you during an audit.

- Respond to IRS notices promptly — Every notice has a deadline. Acting quickly keeps more options open.

Conclusion

Tax debt is a common challenge, and it is a solvable one. Whether you owe back taxes from a single missed payment or have accumulated a larger balance over time, structured programs exist to help you resolve tax debt and move forward.

Acting early almost always leads to better outcomes. The longer a balance sits unresolved, the more penalties and interest grow and the more limited your options become. Resolving tax debt is generally far easier before collection actions escalate to liens or levies.

If your situation feels complex, a tax resolution specialist in Texas or your area can help evaluate your options, communicate with the IRS on your behalf, and find the most favorable path forward.

Frequently Asked Questions

What is considered tax debt?

Tax debt is any amount owed to the federal or state government after your total tax liability exceeds what you paid through withholding, estimated payments, or credits. It includes the original unpaid balance plus any penalties and interest that have accrued since the due date.

Can I pay IRS tax debt in monthly installments?

Yes. The IRS offers installment agreements that allow monthly payments toward your balance. Setting up an IRS payment plan typically prevents collection action while the agreement is active, provided you remain current on payments and future filings.

Does IRS tax debt ever expire?

The IRS generally has 10 years from the date of assessment to collect a tax debt. Once that period ends, the IRS can no longer legally pursue collection. However, certain actions such as submitting an Offer in Compromise or filing for bankruptcy can pause or extend that window. Do not rely on expiration as a strategy without consulting a tax professional.

{kind=link}

{kind=link}

{kind=link}