If you’ve fallen behind on your federal taxes, you’ve probably come across two terms that often cause confusion: tax lien and tax levy. Many people use these terms interchangeably, but they represent different stages of the IRS collection process. Understanding the difference can help you respond appropriately to an IRS notice and choose the right path toward resolving your tax debt.

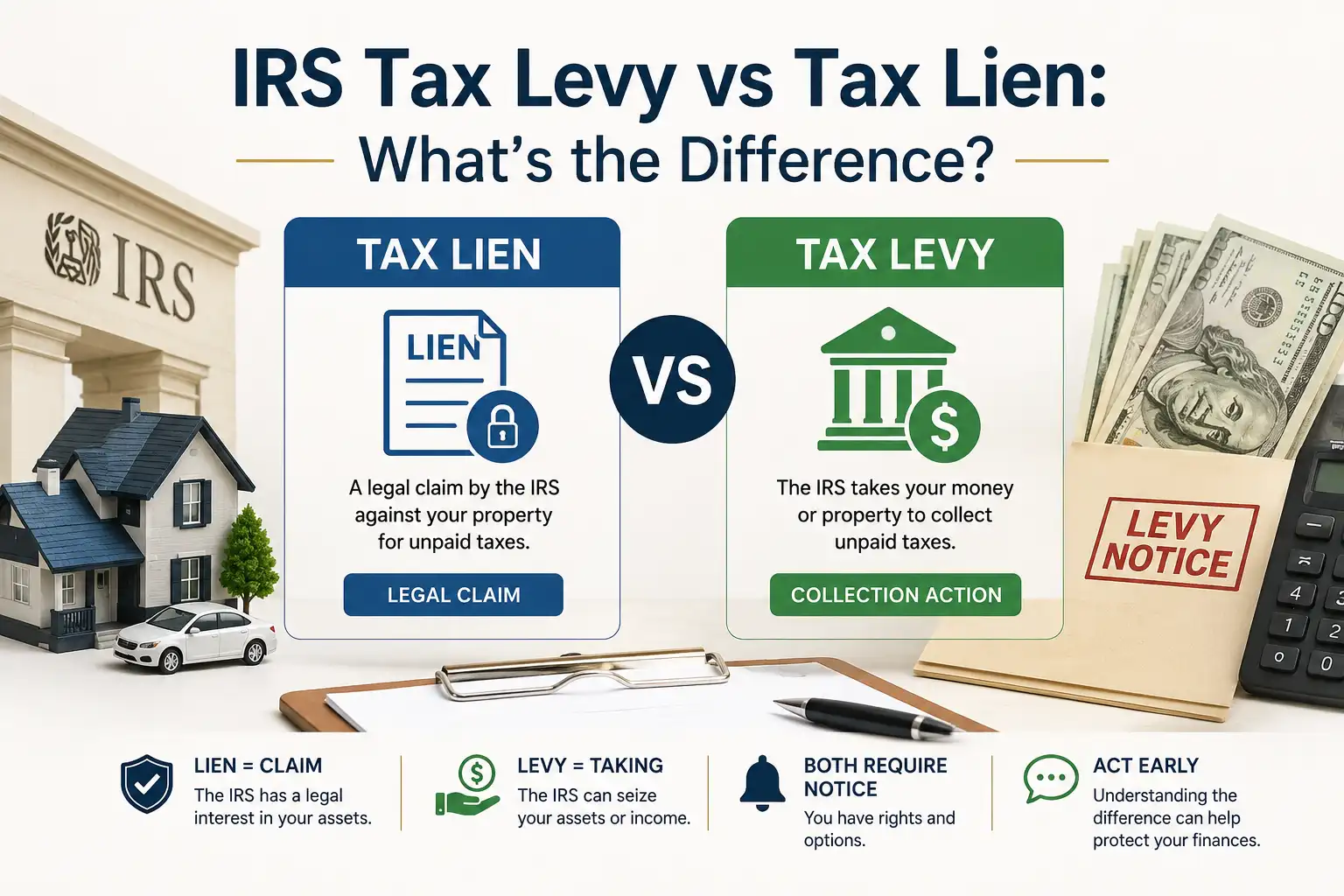

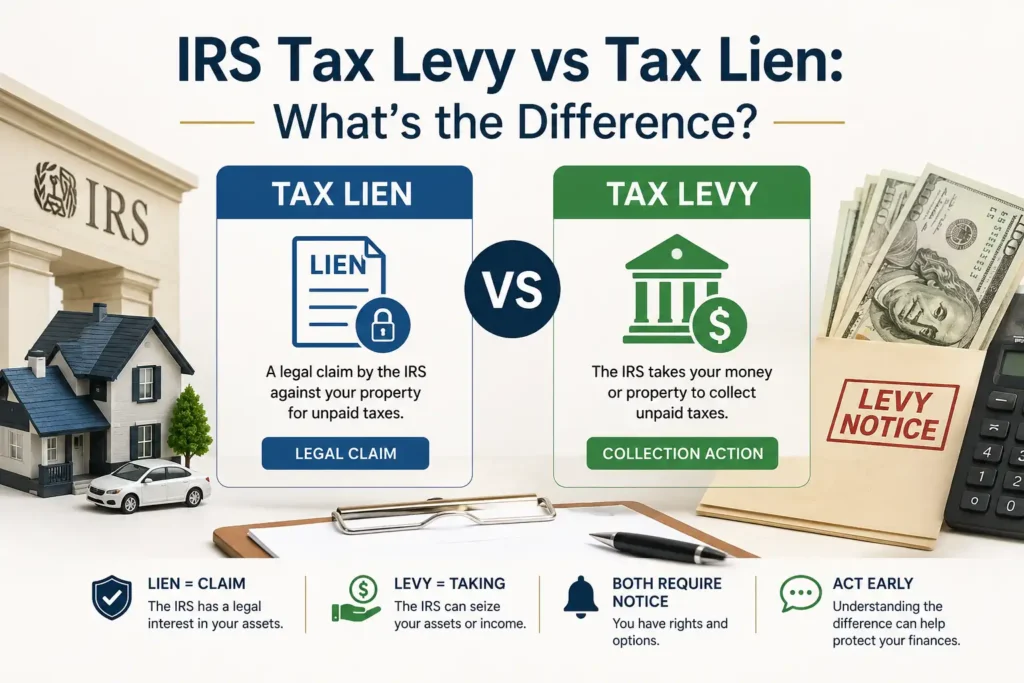

In simple terms, an IRS tax levy allows the Internal Revenue Service (IRS) to seize money or property to collect unpaid taxes, while a Federal Tax Lien is the government’s legal claim against your property because of outstanding tax debt. A lien protects the IRS’s interest in your assets, while a levy is the action taken to recover the balance owed.

This guide explains the differences between the two, outlines the IRS collection process, and reviews the available relief options, including how Karme can help.

IRS Tax Levy vs Tax Lien: A Side-by-Side Comparison

Before looking at each one in detail, here’s a quick comparison.

| Feature | Tax Lien | Tax Levy |

| What it is | A legal claim against your assets | Actual seizure of money or property |

| Impact | Can affect property transactions and financing | Directly removes money or property |

| Requires notice? | Yes, Notice of Federal Tax Lien (NFTL) | Yes, Final Notice of Intent to Levy |

| Can be removed? | Yes, through lien withdrawal, discharge, or release | Yes, through a levy release |

| Severity | Protects the IRS’s legal interest | Active collection action |

Now let’s look at each in more detail.

A Federal Tax Lien is a legal claim the Internal Revenue Service (IRS) places on your property, including your home, vehicle, bank accounts, and other assets, when you have unpaid taxes and have not made arrangements to pay the amount owed.

A lien does not mean the IRS is taking your property. Instead, it establishes the government’s legal interest in your assets until the balance is resolved.

A federal tax lien generally arises after the IRS assesses your taxes, sends a Notice and Demand for Payment, and you do not pay by the due date.

When Does the IRS File a Tax Lien?

The lien attaches to your assets once your tax balance remains unpaid. To make that claim public and notify other creditors, the IRS files a Notice of Federal Tax Lien (NFTL) with the appropriate local or state office.

Filing an NFTL establishes the IRS’s priority claim over your property compared with other creditors, such as banks or mortgage lenders. Once filed, it becomes part of the public record.

How a Tax Lien May Affect Taxpayers

A Federal Tax Lien can affect several areas of your financial life:

- Property transactions: Selling or refinancing property may become more complicated until the lien is resolved.

- Business operations: A lien may attach to business assets, making financing or certain business transactions more difficult.

- Future assets: Property you acquire while the lien remains in effect may also become subject to the lien.

- Borrowing: Some lenders may consider a filed lien when evaluating financing applications.

A tax lien is a serious matter, but it also provides an opportunity to resolve your tax debt before collection actions become more aggressive.

What Is an IRS Tax Levy?

An IRS Tax Levy is the legal seizure of your property to collect unpaid taxes. Unlike a tax lien, which establishes the IRS’s legal claim, a levy allows the IRS to collect directly from your wages, bank accounts, Social Security benefits, or other eligible assets.

A levy is one of the final enforcement actions in the IRS collection process, making it important to respond before it reaches this stage.

When Can the IRS Issue a Tax Levy?

The IRS cannot issue a levy without following specific legal procedures. Before taking action, it must:

- Assess the tax and send a Notice and Demand for Payment.

- Determine that you neglected or refused to pay the balance due.

- Send a Final Notice of Intent to Levy, informing you of your right to request a Collection Due Process (CDP) Hearing, at least 30 days before issuing the levy.

This notice gives you the opportunity to request a CDP hearing, challenge the proposed action, or discuss alternative payment options with the IRS.

If you receive a Final Notice of Intent to Levy, responding within the 30-day period can help protect your rights and preserve your available relief options.

Types of IRS Tax Levies

The IRS may use different types of levies depending on your situation.

- Wage Garnishment: The IRS instructs your employer to withhold part of your paycheck until the tax debt is resolved.

- Bank Account Levy: The IRS may freeze and collect funds from your checking or savings account. Banks generally hold the funds for 21 days before sending them to the IRS, giving you time to seek a resolution.

- Social Security Levy: The IRS may collect a portion of certain Social Security benefits through the Federal Payment Levy Program.

- Property Seizure: In some situations, the IRS may seize and sell assets such as vehicles, real estate, or business property.

- Retirement Account Levy: Although less common, the IRS may levy funds from eligible retirement accounts, including IRAs and 401(k)s.

Tax Levy vs Tax Lien: Key Differences

Here are the key differences between a Federal Tax Lien and an IRS Tax Levy:

- A tax lien is a legal claim against your property, while an IRS tax levy is the actual seizure of your money or assets.

- A lien establishes the IRS’s interest in your property. A levy allows the IRS to collect unpaid taxes.

- A lien may affect property transactions and financing, while a levy can directly remove wages, bank funds, or other assets from your control.

- Both require advance notice from the Internal Revenue Service (IRS). However, once a levy is issued, collection action can begin if no resolution is reached.

IRS Tax Collection Process: From Tax Lien to Tax Levy

Understanding the IRS collection process can help you respond before collection actions become more serious.

- Step 1: Tax Assessment: The IRS assesses your tax liability after you file your return or prepares one on your behalf.

- Step 2: Notice and Demand for Payment: The IRS sends a bill requesting payment of the outstanding balance.

- Step 3: Federal Tax Lien: If the balance remains unpaid, a federal tax lien attaches to your assets.

- Step 4: Notice of Federal Tax Lien (NFTL): The IRS files a public notice to establish its legal claim.

- Step 5: Final Notice of Intent to Levy: You receive a Final Notice of Intent to Levy, giving you at least 30 days to request a Collection Due Process (CDP) Hearing.

- Step 6: IRS Tax Levy: If the issue remains unresolved, the IRS may begin collecting through wage garnishment, a Bank Account Levy, or Property Seizure.

Understanding where you are in this process makes it easier to evaluate your available tax resolution options.

Can an IRS Tax Lien Be Removed?

Yes. A Federal Tax Lien may be released, withdrawn, or discharged in several situations.

- Pay the full tax debt: The lien is generally released after the balance, including penalties and interest, is paid.

- Lien withdrawal: The IRS may withdraw the lien from the public record in qualifying situations, including certain Installment Agreement arrangements.

- Offer in Compromise (OIC): If your Offer in Compromise is accepted and completed, the lien is typically released.

- Property discharge: The IRS may remove the lien from a specific property to allow a sale or transfer.

- Collection statute expiration: In some cases, the lien ends when the IRS collection period expires.

Removing a lien often requires careful planning, which is why many taxpayers seek professional IRS Tax Resolution assistance.

Can an IRS Tax Levy Be Released?

Yes. A Levy Release is possible when specific IRS requirements are met. The IRS may release a levy if:

- You pay the full amount owed.

- The levy creates financial hardship.

- You enter into an eligible Installment Agreement or one of the available IRS Payment Plans.

- Your Offer in Compromise is accepted.

- The levy was issued in error or required procedures were not followed.

- The IRS collection period has expired.

If your wages are being garnished or your bank account has been levied, acting quickly can improve your chances of resolving the issue before additional collection actions occur.

Options for Resolving IRS Tax Debt

If you’re dealing with a Federal Tax Lien, an IRS Tax Levy, or growing tax debt, several IRS programs may help resolve your balance.

Installment Agreements

An Installment Agreement, commonly called one of the IRS Payment Plans, allows you to pay your tax debt through affordable monthly payments. Depending on your situation, setting up a payment plan may help prevent a levy and, in some cases, support a Lien Withdrawal.

Learn more about IRS Payment Plans to determine which option best fits your financial situation.

Offer in Compromise

An Offer in Compromise (OIC) allows eligible taxpayers to settle their tax debt for less than the full amount owed. The IRS reviews your income, expenses, assets, and ability to pay before approving an application.

While not everyone qualifies, an Offer in Compromise can provide meaningful tax relief for eligible taxpayers.

Currently Not Collectible Status

If paying your tax debt would create financial hardship, you may qualify for Currently Not Collectible (CNC) status. This temporarily pauses IRS collection actions, including certain levies, until your financial condition improves.

Interest and penalties may continue to accrue while your account is in CNC status, and the IRS will review your financial situation periodically.

Penalty Relief

The IRS may reduce or remove certain penalties through Penalty Abatement if you have reasonable cause or qualify under the First-Time Penalty Abatement program. This can reduce your overall tax debt and make resolving your balance more manageable.

When Should You Seek Professional Tax Resolution Assistance?

Handling IRS collection matters on your own can be challenging, especially when multiple notices or enforcement actions are involved.

You may benefit from professional assistance if:

- You’ve received a Notice of Federal Tax Lien (NFTL).

- You’ve received a Final Notice of Intent to Levy.

- Your wages are being garnished or your bank account has been levied.

- You owe more than you can reasonably afford to pay.

- You’re considering an Offer in Compromise.

- You need to request a Collection Due Process (CDP) Hearing before the deadline.

Karme helps individuals, families, and business owners address IRS tax matters with practical guidance and personalized support. Our licensed tax professionals work directly with the Internal Revenue Service (IRS) to identify the most appropriate solution, whether that involves IRS Payment Plans, an Offer in Compromise, a Levy Release, or other available tax relief programs. Our goal is to help you resolve your tax obligations efficiently while protecting your financial future.

Frequently Asked Questions

Is a tax levy more serious than a tax lien?

Yes. A Federal Tax Lien is a legal claim against your property, while an IRS Tax Levy is the actual collection of money or assets. Because a levy directly affects your finances, it is generally considered the more serious enforcement action.

Does every tax lien lead to a tax levy?

No. Many taxpayers resolve their tax debt through Installment Agreements, IRS Payment Plans, or an Offer in Compromise before the IRS takes levy action.

Can the IRS remove a tax lien?

Yes. Depending on your circumstances, the IRS may release, withdraw, discharge, or subordinate a Federal Tax Lien after payment or through other qualifying resolution programs.

How can I stop an IRS tax levy?

If you’ve received a Final Notice of Intent to Levy, you may request a Collection Due Process (CDP) Hearing within 30 days. Entering into an eligible payment arrangement or working with a tax professional may also help prevent or resolve a levy.

How long do IRS tax liens and levies remain in effect?

A Federal Tax Lien generally remains in effect until the tax debt is paid, released, or the IRS collection period expires. An IRS Tax Levy continues until the debt is resolved or the IRS issues a Levy Release.

Conclusion

A Federal Tax Lien and an IRS Tax Levy represent different stages of the IRS collection process. A lien establishes the IRS’s legal interest in your property, while a levy allows the agency to collect unpaid taxes from your income or other assets.

Fortunately, taxpayers have several options to address outstanding tax obligations, including IRS Payment Plans, an Offer in Compromise, Currently Not Collectible (CNC) status, and other IRS relief programs. Taking action early can help prevent additional collection measures and improve your chances of reaching a favorable outcome.

If you’re dealing with an IRS Tax Levy, Federal Tax Lien, or other IRS collection matters, Karme’s experienced tax professionals can help you understand your options and identify the solution that best fits your situation.

{kind=link}

{kind=link}

{kind=link}