Owing the IRS a significant amount of money is one of the most stressful financial situations a person can face.

And if that balance has crossed $25,000, the stakes are even higher. At this threshold, the IRS’s collection tools become more aggressive, and your options narrow the longer you wait.

The good news is that solutions exist. And with the right support from a trusted tax professional like Karme, even a serious IRS debt can be resolved.

That said, here is what happens if you owe the IRS more than $25,000, and what you can do about it.

What Happens If You Owe the IRS More Than $25,000: Key Consequences

The $25,000 amount is a firm limit in IRS collection rules, after which the agency uses more intense ways to collect the debt you owe. Typically, you will receive several notices about the tax you owe, including a Notice of Deficiency. If you don’t respond, the IRS will use more aggressive actions to collect the money.

Below are the specific steps the IRS can take to handle a large tax debt.

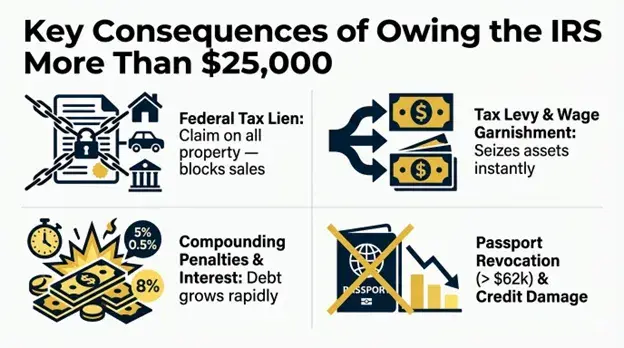

Federal Tax Lien

A federal tax lien is one of the first major actions from the IRS. It is a legal claim the IRS places on everything you own. This will typically include your home, land, vehicles, bank accounts, and retirement savings.

Once the lien is filed, it becomes attached to your property titles. For example, if you try to sell your house, the sale cannot be completed until the IRS is paid from the proceeds. That’s because the IRS is legally entitled to take its share of the money before the homeowner receives anything.

Tax Levy and Wage Garnishment

If you don’t respond to IRS notices, another powerful tool the IRS can use is a tax levy, which is different from a lien. A lien simply establishes the government’s legal claim, while a levy actually takes the money or property to satisfy the debt.

The IRS can also order your employer to send part of your paycheck to the government before you receive it. This is known as wage garnishment. In addition, the IRS may remove funds from your bank account or seize money held in investment accounts to satisfy the debt.

Compounding Penalties and Interest

As you delay paying your tax debt, the amount owed continues to grow because of penalties and interest. Two separate penalties can apply at the same time.

- Failure-to-file penalty: 5% of the unpaid tax for each month the tax return is late, up to a maximum of 25% of the original amount owed.

- Failure-to-pay penalty:5% per month, also capped at 25%.

In addition to these, the IRS charges interest at an annual rate of about 8%. And this interest compounds daily. For a tax debt of $25,000, interest alone can add more than $2,000 each year, even before including the penalties.

Passport Revocation and Credit Damage

If your balance rises above $62,000, the IRS can notify the U.S. State Department that the taxpayer has a seriously delinquent debt. As a result, the State Department can deny you a new passport application or even revoke an existing passport.

In addition, when the IRS files a federal tax lien, it becomes part of the public record. This will significantly lessen your credit score. As a result, it you won’t be able to qualify for loans, rent an apartment, or run a business that depends on credit.

How to Handle Large IRS Debt If You Cannot Pay

If you cannot pay the full amount right away, there are ways to manage this critical situation. The IRS offers several ways to resolve large tax debts, and early action dramatically improves your outcomes.

Let’s review these options in detail.

Installment Agreements (IRS Payment Plans)

For debts between $25,000 and $50,000, the most straightforward option is a non-streamlined installment agreement. It is one of the most widely used IRS payment plans available. Based on this, you get up to 72 months to repay, but you must either agree to direct debit or submit Form 433-F.

For balances over $50,000, a full Collection Information Statement is required, and the IRS exercises greater discretion over terms. IRS FY 2024 Data Book reports the agency collected over $16 billion through installment agreements in FY 2024, which is more than 12% higher than the previous year. This shows that this is the most commonly used resolution path for taxpayers.

Offer in Compromise (OIC)

An Offer in Compromise allows certain taxpayers to settle their tax debt for less than the full amount they originally owed. However, qualifying for this program is difficult. Before approving an application, the IRS carefully reviews your income, monthly expenses, and asset equity to determine what you can realistically pay. Although it is a legitimate option, it is not an easy one.

According to the IRS FY 2024 Data Book, the IRS approved only 7,199 OIC applications out of total 33,591 received. This means that roughly 21% of applicants were accepted. Because the application process requires detailed financial information and strict documentation, many taxpayers choose to seek professional tax preparation services to prepare the application properly and improve their chances of approval.

Currently Not Collectible (CNC) Status

If you’re wondering, what happens if I owe more taxes than I can pay, CNC status might be your solution. This requires that you genuinely cannot meet basic living expenses and pay your tax debt. When the IRS grants this status, it temporarily stops active collection actions. However, this does not relieve your debt.

However, you will still owe the full amount, and interest and penalties will continue to accumulate over time. Also, the IRS will review your financial situation periodically. You can obtain CNC status by submitting Form 433-A with supporting financial documentation.

Penalty Abatement

If you have a clean compliance record, meaning no penalty notices in the past three years, you may qualify for first-time penalty abatement (FTA). This can eliminate failure-to-file or failure-to-pay penalties entirely. However, it does not reduce the underlying tax owed or interest charges.

Also, penalty abatement is different from other tax resolution services that focus on reducing the main tax balance. Even so, having the penalties removed can still lower the total amount you need to pay by a significant margin.

Final Words: Take Action Before the IRS Does

Now you know exactly what happens if you owe the IRS more than $25,000. At this balance, the IRS can use formal collection methods. Fortunately, you still have options to pay the debt or lower the amount owed. The key is to take action early, as any delay will cause the penalties and interest to keep accumulating.

That’s why it’s best to work with a tax professional who can guide you through the process. Karme specializes in exactly this situation. We will negotiate with the IRS on your behalf, ensure penalty relief, and set up the best payment plan that works for you. Contact us today to discuss your situation and find the best resolution path.

{kind=link}